FIRE Movement Guide. Imagine waking up on a Tuesday morning and having absolutely nowhere you have to be. No alarm. No commute. No boss waiting for that report. Just-time. Your time.That’s not a fantasy. For thousands of people around the world, that’s just a regular Tuesday. They didn’t win the lottery. They didn’t inherit a fortune. They discovered the FIRE Movement-and they followed the plan.

This guide covers everything. From understanding what FIRE actually means, to the different types of FIRE strategies, to the exact calculations you need, to the investments that grow your wealth, to the lifestyle adjustments that make it all possible. Every section below links to a dedicated deep-dive post so you can explore exactly what matters to you.

Let’s start at the beginning.

FIRE Movement Guide: What Is Financial Independence?

The FIRE Movement was popularized in the 1990s through the book Your Money or Your Life by Vicki Robin and Joe Dominguez. But it truly exploded online through communities like r/financialindependence and the iconic Mr. Money Mustache blog – which showed regular people how to retire in their 30s.

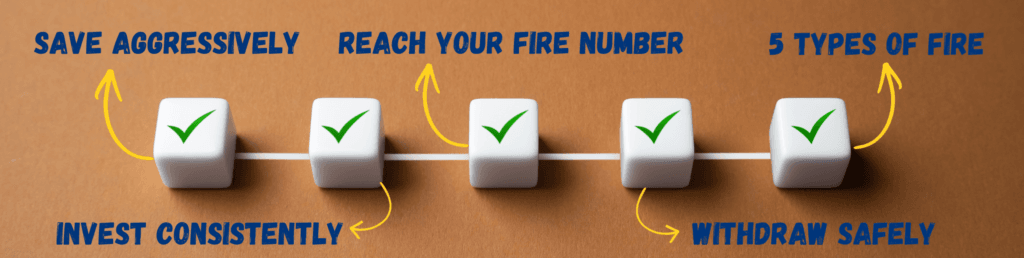

The core FIRE framework is built on four pillars:

- Save aggressively – typically 50-70% of your take-home income

- Invest consistently – mainly in low-cost index funds and passive assets

- Reach your FIRE Number – 25x your annual expenses

- Withdraw safely – using the 4% rule to fund your lifestyle indefinitely

The 5 Types of FIRE – Which One Matches Your Life?

Here’s something the FIRE community figured out quickly: one size does not fit all. A 28-year-old minimalist living in Vietnam has a completely different FIRE plan than a 42-year-old with three kids in a high cost-of-living city.

That’s why FIRE evolved into five distinct strategies. Understanding which type fits your life is arguably the most important decision you’ll make on this journey.

| FIRE Type | Best For | Annual Spend Target | Key Idea |

| Lean FIRE | Minimalists, frugalists | Under $40,000/year | Live on very little, retire very fast |

| Fat FIRE | High earners, lifestyle lovers | $100,000+/year | Retire comfortably without sacrificing comfort |

| Barista FIRE | Social people, part-time lovers | $25,000–$50,000/year | Semi-retire; part-time work covers extras |

| Coast FIRE | Young investors with time | Varies | Invest early, let compounding do the rest |

| Slow FIRE | Burnout-avoiders, gradual reducers | Varies | Reduce work slowly – no rush, no pressure |

Coast FIRE vs Lean FIRE – The Most Common Debate

This FIRE Movement Guide. These two get compared constantly, and for good reason – they represent opposite ends of the FIRE spectrum. Lean FIRE is about cutting your lifestyle to the bone so you can retire as fast as possible. Coast FIRE is about investing early and then coasting – letting time and compound interest do the heavy lifting while you work normally (or barely at all).

Neither is better. It depends entirely on what kind of life you want to live right now, not just in retirement.

🔗 Read More: Coast FIRE vs Lean FIRE: Which Path is Right for You?

Barista FIRE – Work Part-Time, Live Full-Time

Barista FIRE is one of the most popular middle-ground strategies. The idea is that you don’t need to fully retire to be financially free. You reach a point where your investments cover most of your expenses – and a small part-time job (like, famously, working at Starbucks for the health benefits) covers the rest.

It’s a softer landing. Less pressure. And for many people, especially those who enjoy some structure in their week, it’s the perfect balance between work and freedom.

🔗 Read More: Barista FIRE Guide: Retirement with a part-time job.

Fat FIRE – Early Retirement Without Giving Up Comfort

Not everyone wants to retire on a shoestring budget. Fat FIRE is for high earners who want to maintain a generous lifestyle in retirement – nice vacations, good restaurants, private schools for the kids. The FIRE number is significantly higher (often $2.5M–$4M+), but so is the quality of retirement life.

🔗 Read More: What is Fat FIRE? Strategy for a luxury retirement.

Slow FIRE – The Burnout-Friendly Approach

Slow FIRE rejects the aggressive savings rates of traditional FIRE and instead advocates for a gradual, sustainable path. You reduce your working hours progressively. You enjoy life during the journey, not just at the destination. It’s FIRE for people who’d rather walk than sprint – and there’s absolutely nothing wrong with that.

🔗 Read More: Slow FIRE Explained: Achieving freedom without burnout.

🔗 Read More: FIRE Movement Types: 5 ways to retire early in 2026.

The Numbers Behind FIRE – What You Actually Need to Retire Early

This is where most people either get excited or get intimidated. The math behind FIRE looks complicated at first glance. But once you break it down, it’s actually one of the clearest financial roadmaps you’ll ever follow.

Your FIRE Number – The Most Important Figure in Your Financial Life

FIRE Number = Annual Expenses × 25

That’s it. If you spend $40,000 a year, your FIRE number is $1,000,000. If you spend $60,000, it’s $1,500,000. The formula never changes – only your spending does.

And here’s the most motivating thing about this math: every dollar you cut from your annual spending reduces your FIRE number by $25. Cut $200/month from your budget and your FIRE number drops by $60,000. That’s not small.

| Annual Spending | Your FIRE Number | Years to FIRE (saving 50%, 7% returns) |

| $25,000/year | $625,000 | ~12 years |

| $40,000/year | $1,000,000 | ~17 years |

| $60,000/year | $1,500,000 | ~21 years |

| $80,000/year | $2,000,000 | ~24 years |

| $100,000/year | $2,500,000 | ~27 years |

🔗 Read More: Calculate Your FIRE Number: A simple 5-minute guide.

The 4% Rule in 2026 – Still Reliable?

The 4% rule comes from the Trinity Study – a landmark piece of research showing that withdrawing 4% of your portfolio annually has historically sustained a 30-year retirement across various market conditions.

But in 2026, people are asking fair questions: Is inflation killing the 4% rule? Does it hold for a 50-year retirement, not just 30? The honest answer – it still works as a starting guideline, but longer retirements may call for a slightly more conservative 3.5% withdrawal rate.

The full breakdown of this – including updated research and how it applies to your specific timeline – is in the dedicated post below.

🔗 Read More: Is the 4% Rule Safe? Withdrawal strategies for 2026.

FIRE on a $50,000 Salary – Yes, It’s Possible

This FIRE Movement Guide, this is the post most people need to read. Because the biggest myth in the FIRE world is that you need a tech salary or a side hustle empire to retire early. You don’t.

A $50,000 salary with disciplined spending and consistent investing can absolutely get you to FIRE. It takes longer. It requires more intentionality. But it works. The math doesn’t discriminate by income – it rewards savings rate.

🔗 Read More: FIRE on a $50k Salary – A Realistic and Inspiring Roadmap

Retire at 45 With $500,000 – Is It Enough?

$500,000 sounds like a lot.FIRE Movement Guide, But is it actually enough to retire at 45 – potentially for 40+ years? The answer depends entirely on your annual spending and where you live. Combined with geographic arbitrage or a Barista FIRE approach, $500,000 can absolutely be a retirement springboard.

🔗 Read More: Retire at 45 with $500k: Is it actually possible?

The FIRE Emergency Fund – Cash You Can’t Skip

Every FIRE plan needs a cash buffer. A 6–12 month emergency fund sitting in a high-yield savings account isn’t dead money – it’s your shield. It means you don’t have to sell investments at a loss when life throws a curveball, and it means sequence-of-returns risk doesn’t derail your entire retirement.

🔗 Read More: FIRE Emergency Fund – How Much Cash Should You Keep Aside?

How to Invest for FIRE – Building the Portfolio That Sets You Free

Saving money is step one. But savings alone won’t get you to FIRE. Inflation will quietly eat your cash over decades. You need your money growing – and that means investing.

The FIRE community has developed a strong consensus on this: low-cost index funds are the foundation of almost every successful FIRE portfolio. They’re passive, diversified, and historically one of the highest-performing long-term investments available to ordinary people.Use this FIRE Movement Guide to calculate exactly how much money you need to retire.

Best Index Funds for FIRE – Safe, Long-Term, Boring (In the Best Way)

Index funds track an entire market – like the S&P 500 or the total US stock market. You’re not picking individual stocks. You’re owning a tiny piece of hundreds or thousands of companies at once. When the market grows, you grow with it.

- Vanguard Total Stock Market Index Fund (VTSAX) – the FIRE community favourite

- Fidelity ZERO Total Market Index Fund – 0% expense ratio

- Schwab Total Stock Market Index (SWTSX) – low cost, highly accessible

🔗 Read More: Best Index Funds for FIRE: Top low-cost picks for 2026.

Real Estate vs Stocks for FIRE – Which Wins?

This is one of the great FIRE debates. Real estate gives you leverage, cash flow, and tax advantages. Stocks give you liquidity, diversification, and complete passivity. The best answer for most people? Both – in the right proportion for your risk tolerance and time horizon.This FIRE Movement Guide proves that early retirement is not just for the wealthy.

| Factor | Index Funds / Stocks | Real Estate |

| Liquidity | ✅ High – sell anytime | ❌ Low – takes months to sell |

| Passive-ness | ✅ Fully passive | ⚠️ Requires management |

| Leverage | ❌ Not typical | ✅ Mortgage amplifies returns |

| Cash Flow | ⚠️ Dividends only | ✅ Monthly rental income |

| Barrier to Entry | ✅ Start with $1 | ❌ Needs significant capital |

| Tax Advantages | ⚠️ Capital gains tax | ✅ Depreciation, 1031 exchange |

🔗 Read More: Real Estate vs Stocks for FIRE – Which Is Better for Early Retirement?

Passive Income for FIRE – Making Money While You Sleep

The dream of FIRE isn’t just a large portfolio – it’s multiple income streams that flow in without your active effort. Dividends from stocks. Rental income. Digital products. Royalties. Each stream reduces how much you need to withdraw from your portfolio, extending its life dramatically.

🔗 Read More: Passive Income for FIRE: 7 ways to earn while you sleep.

Tax-Free FIRE Withdrawals – The Legal Way to Pay Less

One of the most overlooked parts of FIRE planning is how you withdraw money, not just how you save it. Roth IRA ladders, tax-loss harvesting, and strategic Roth conversions can legally reduce your tax bill to near zero in early retirement. This isn’t a loophole – it’s the tax code working as designed.

🔗 Read More: Tax-Free FIRE Hacks: Legal ways to keep more of your money.

Low-Cost ETFs for FIRE – The Cheapest Way to Grow Wealth

ETFs (Exchange-Traded Funds) work like index funds but trade on stock exchanges like individual stocks. The key advantage for FIRE investors? Ultra-low expense ratios. Paying 0.03% in fees instead of 1% sounds small – but over 20 years, it can mean hundreds of thousands of dollars more in your portfolio.

🔗 Read More: Best Low-Cost ETFs: Build wealth with minimal fees.

The FIRE Lifestyle – What Nobody Warns You About

The financial community talks endlessly about the numbers. The savings rate. The withdrawal strategy. The index funds. But there’s a whole other side of FIRE that doesn’t show up in any spreadsheet – and it catches a surprising number of people completely off guard.

What do you actually do when you retire early?

Identity. Purpose. Structure. Social connection. These aren’t soft topics – they’re the difference between a retirement that feels like freedom and one that quietly feels like something’s missing. The FIRE lifestyle is real, but it has to be designed just as intentionally as the financial plan.

FIRE for Single Parents – Harder, But Absolutely Possible

Single parents face a FIRE challenge that most guides completely ignore: you’re running on one income, supporting more than one person, with less flexibility to take risks. The FIRE number needs to be more conservative. The emergency fund needs to be larger. But with the right plan, single parents are absolutely achieving FIRE – and their stories are some of the most inspiring in the community.

🔗 Read More: FIRE for Single Parents: Managing solo on the path to freedom.

Geographic Arbitrage – The Fastest Way to Shrink Your FIRE Number

Here’s a strategy that can cut your FIRE number by 40–60%: move somewhere cheaper.

Geographic arbitrage means earning (or having saved) money in a high-income country’s currency while living in a country with significantly lower costs. Portugal, Thailand, Mexico, Colombia – there are dozens of countries where a $2,000/month budget funds a genuinely comfortable lifestyle.

If your FIRE number in the US is $1,500,000, geographic arbitrage might bring that down to $600,000. Same freedom. Much faster timeline.

🔗 Read More: Geographic Arbitrage: Move to a cheaper city and retire now.

Life After Early Retirement – Mental Health and Finding Purpose

This is the post most FIRE resources skip. And it might be the most important one.

A significant number of early retirees report feeling lost, bored, or purposeless in their first year of retirement. When work disappears, so does structure, social connection, and the daily sense of accomplishment. This doesn’t mean FIRE was a mistake – it means the transition needs to be managed.This FIRE Movement Guide proves that early retirement is not just for the wealthy.

Build a life before you leave work. Know your hobbies. Have a community. Have something you’re moving toward, not just something you’re running away from.

🔗 Read More: Life After FIRE: What to do once you actually retire?

Common FIRE Mistakes That Delay Early Retirement

People fail at FIRE not because the strategy doesn’t work – but because they make predictable, avoidable mistakes. Here are the biggest ones:

- Underestimating healthcare costs – especially in countries without universal coverage. This alone can derail a FIRE plan.

- Ignoring inflation – your FIRE number needs to account for 30–40 years of rising costs.

- Lifestyle inflation – as your income grows, so does your spending. This pushes your FIRE number further every year.

- No emergency fund – selling investments during a market dip to cover emergencies is one of the fastest ways to ruin a FIRE plan.

- Sequence-of-returns risk – retiring right before a major market crash can permanently damage your portfolio if you’re not withdrawing carefully.

- Burning out before you get there – extreme frugality and intense saving are unsustainable for most people. Balance matters.

🔗 Read More: 7 Common FIRE Mistakes: Don’t let these delay your retirement.

🔗 Read More: Top 5 FIRE Books: Must-read reviews for every investor.

Conclusion – Your FIRE Journey Starts Today

Look, nobody is coming to save you from a 40-year career you didn’t choose.

No government policy. No lucky break. No viral moment.

The only way out is a plan – and This FIRE Movement Guide is the clearest, most proven plan ordinary people have ever had access to.

You’ve now seen the full picture:

- The 5 FIRE types – so you can pick the one that actually fits your life

- The exact numbers – your FIRE number, the 4% rule, real salary-based examples

- The investments – index funds, ETFs, real estate, passive income, tax strategies

- The lifestyle reality – single parent FIRE, geographic arbitrage, life after retirement, and the mistakes that slow people down

This isn’t theory. People on $40,000 salaries are doing this. Single parents are doing this. People in their 50s who started late are doing this.

This FIRE Movement Guide is not just another article about saving money. It is a complete roadmap built for real people living in the real world — people with bills, responsibilities, self-doubt, and big dreams at the same time. Whether you are starting from zero or already halfway there, the FIRE Movement meets you exactly where you are.

This FIRE Movement Guide, the path to financial independence is not always straight. Some months you will crush your savings goal. Other months life will happen — an unexpected expense, a bad market week, a moment where quitting feels easier than continuing. That is completely normal. Every single person who achieved FIRE went through the same doubts.This FIRE Movement Guide proves that early retirement is not just for the wealthy.

What separates the ones who made it? They kept going anyway.

So save this FIRE Movement Guide, share it with someone who needs it, and revisit it every time you feel lost. Your financially free future is being built right now — one decision, one investment, and one skipped impulse purchase at a time.

The best time to start was yesterday. The second best time is today. 🔥

Pick one thing from this guide. Do it this week. Open that brokerage account. Calculate your FIRE number. Cut that one subscription you forgot about.This FIRE Movement Guide shows that retiring early is about smart decisions, not a huge salary.

Small moves. Consistent direction. Radical patience.

That’s the whole game. 🔥 of This FIRE Movement Guide.